We’re excited to launch ratings for crypto liquidity providers. This rating system is designed to bring transparency and rigor to one of the most important — and least standardized — areas of digital asset counterparty risk management.

Liquidity providers are critical nodes in the crypto market’s infrastructure. They support market-making, OTC liquidity, execution services, prime brokerage, and other institutional liquidity channels. Yet many of these firms operate through private trading relationships, exchange agreements, and proprietary infrastructure, leaving institutions with fewer public data points than they have for exchanges, custodians, or stablecoin issuers.

Despite the role that liquidity providers play, the tools to assess their risks have been limited. The market needs standardized and quantifiable metrics to assess and compare liquidity provider default risk.

A Quantitative Leap Forward

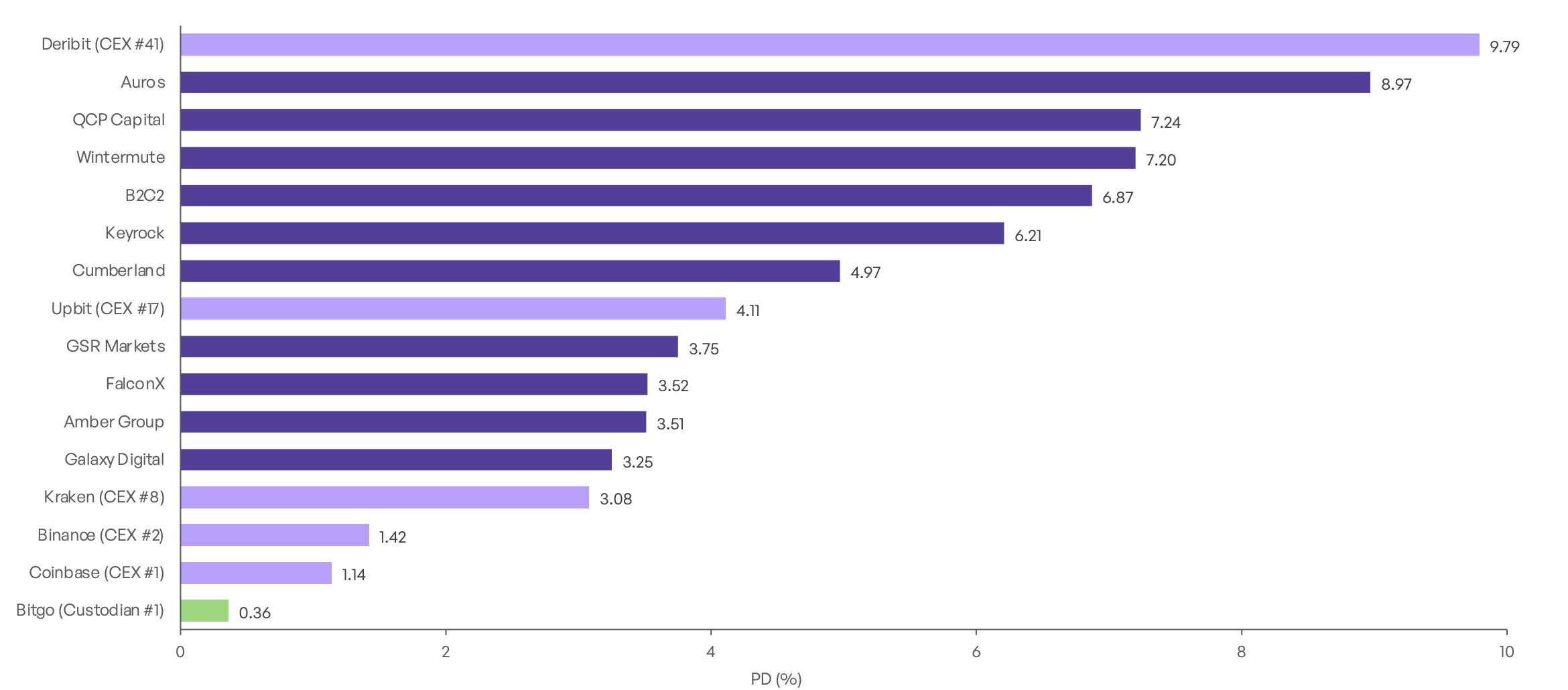

Agio Ratings’ LP Statistical Ratings are derived from a proprietary risk model for liquidity providers. The model measures one-year probability of default using a statistical approach informed by prior industry defaults, similar in structure to Agio Ratings’ existing CEX Statistical Ratings.

Because liquidity providers are often less transparent than other counterparties, Agio Ratings’ methodology combines available off-chain information with observable on-chain behavior. This allows Agio Ratings to develop a consistent view of liquidity provider risk even where traditional financial disclosure is limited.

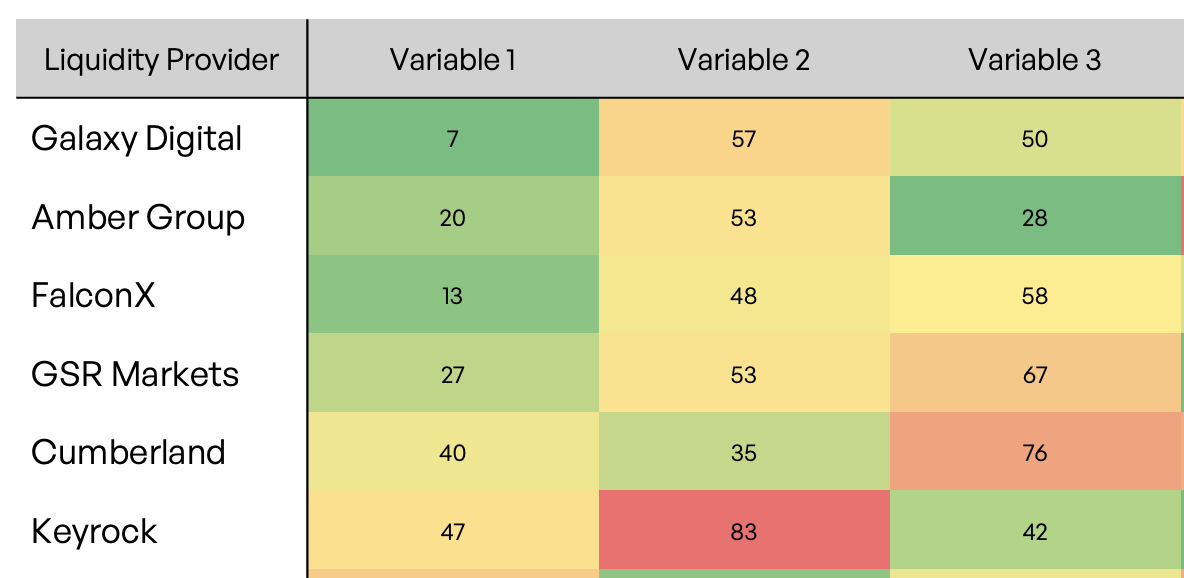

The result is a data-driven view across a first cohort of major liquidity providers — giving institutions a clearer lens into where liquidity provider risk is concentrated, where resilience appears stronger, and where further counterparty diligence may be required.

Built for an Opaque Market

Liquidity provider risk is difficult to evaluate because many of the most important firms in the market are privately held, institutionally focused, and not subject to standardized disclosure requirements.

Agio Ratings’ approach is designed specifically for this environment. The model evaluates a broad universe of observable risk indicators across business profile, market behavior, operational footprint, and on-chain activity. These indicators are tested against historical industry stress events and transformed into a comparable one-year probability of default.

This allows users to compare liquidity providers using a common risk framework, rather than relying solely on anecdotal market color, bilateral disclosures, or fragmented internal assessments.

The ratings also reflect Agio Ratings’ broader commitment to building credit risk infrastructure for the digital asset market: transparent enough to support institutional decision-making, while preserving the integrity of the proprietary models that power the analysis.

Benchmark Your Liquidity Provider Risk

Agio Ratings’ Liquidity Provider Ratings are now live, giving institutions a standardized way to compare default risk across key crypto liquidity providers.

Use the ratings to support counterparty reviews, trading limits, risk monitoring, and internal credit assessments — especially in a market where disclosure remains limited and private relationships often obscure the full risk picture.

Book a Demo to Benchmark Your LP Exposure