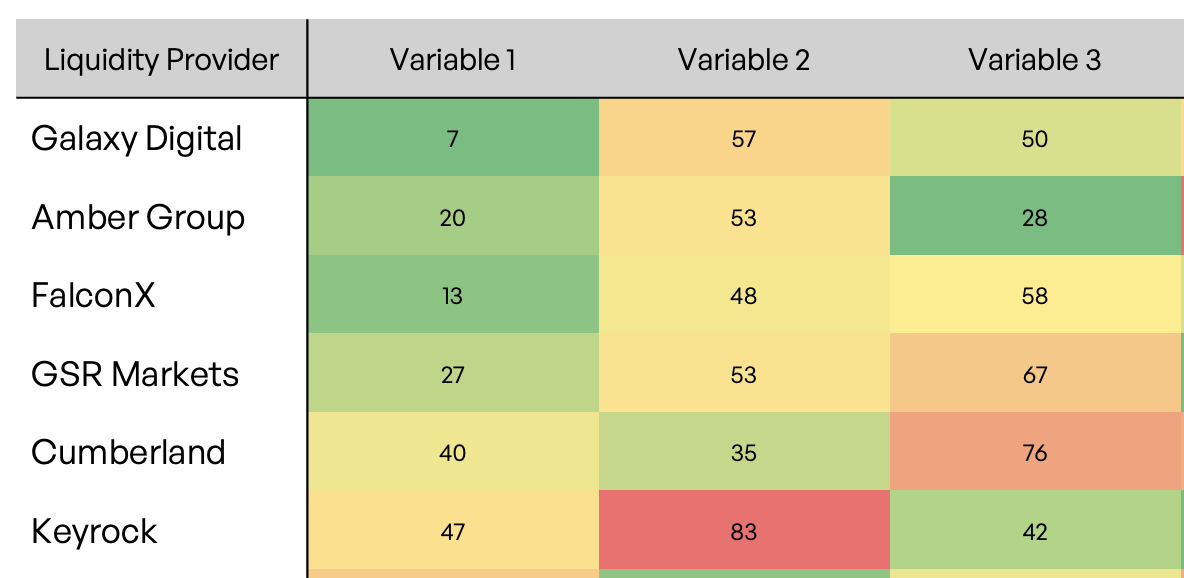

In line with this quote from Chi Chi Rodríguez, the professional golfer, it’s the received wisdom that crypto-trading volumes are grossly inflated. But to what extent? And who are the main protagonists? A quick Google search yields fairly wild claims like “95% of crypto-volumes are wash-trades” and sometimes even higher. We estimate 60% and here’s why….

When you suspect shenanigans, it’s useful to ask “Cui Bono” or who gains? Accordingly, the most frequently cited reason for inflated crypto volumes is people trying to improve an exchange ranking. Hence Coingecko provide a Normalized-Reported Volume, where they’ve adjusted reported trading volumes using SimilarWeb traffic estimates, and then they use that in their Trust Score.

Looking at a recent sample of data, Coingecko only normalise 17% of the 430 exchanges they’re tracking. It seems unlikely that the extent of wash-trading is that limited. So we replicated that analysis in the graphic above using median SimilarWeb traffic and Coingecko trading volumes, converted into Bitcoin equivalent, over the same six months. As you can see, there’s a relationship, though the R-Sq is just 8%.

Interestingly there is also a “frontier” in the data defined by the more estalished retail exchanges, like Binance, Coinbase, FTX and Gemini. By implication, anyone north of that frontier line is reporting more volumes than their web traffic would imply. Almost by definition this would apply, in varying degree, to almost all the exchanges. Certainly a lot more than 17% of them.

There are other legitimate reasons for exchanges to be above this frontier. For example, ZBG might mostly trade wholesale and have relatively little retail volume in its mix. When you use the frontier line to estimate the amount of retail volume across all the exchanges you get about BTC500k per day. What should you add to account for those wholesale volumes?

A recent BNY Mellon report* estimated the amount of retail volume in US Equities at 25% (amazingly up from 10% a few years ago before the pandemic). Allowing for the lower levels of institutional trading in crypto, you might estimate the equivalent figure at 50%, yielding BTC1,000k per day for the entire market. The reported volumes in this sample are BTC2,500k per day so that means BTC1,500k, or 60%, are wash-trades.

Our estimate is comfortingly similar to Cong et al. (2021)** who estimated wash-trading at 70% using a bottom-up methodology to identify abnormal first-significant-digit distributions, size rounding, and transaction tail distributions. Clearly this is a massive amount of wash-trading. But the headline, as so often is the case with digital assets, is that it’s bad, just not as bad as everyone thinks.

* The Rise of Retail Traders. BNY Mellon https://www.bnymellonwealth.com/articles/strategy/the-rise-of-retail-traders.jsp

** Cong, L. W., Xi, L.,Tang, K. & Yang, Y. (2021). Crypto Wash Trading. Cornell University Electronic Journal https://doi.org/10.48550/arXiv.2108.10984