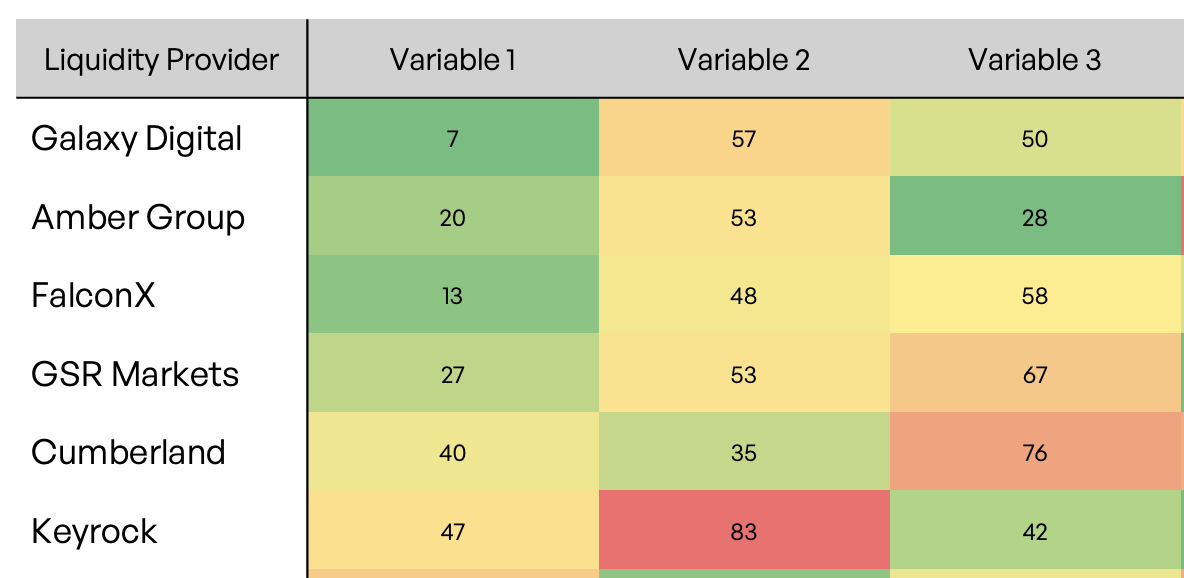

It’s generally agreed that location is an important consideration in counterparty risk. If you are registered and regulated in North America, you are seen as safer than someone based in Palau. But how do you convert this intuition into a number that can be used for managing risk exposure? It’s not as easy as it may sound.

Nexo is a good example of the borderless crypto-globe in which we operate. Based on our research, the firm has legal entities in at least five countries. Most of the staff are apparently in Bulgaria. Most of the customers are in North America. It holds a US FinCen licence, one of the harder regulatory approvals to obtain. Its terms and conditions are subject to the laws of England and Wales. Where are they?

Our early attempts to quantify location haven’t been predictive of default. For example, the World Bank’s Governance Indicator includes a Regulatory Quality measure. Germany and the Bahamas score 92.5 and 47.2, respectively. You can allocate this score to crypto counterparties based on where they have staff, customers or legal entities. Unfortunately, none of these location-weighted Regulatory Quality metrics seem to work.

We think our problem is granularity. Germany is generally well regulated, but how hard is it to register with the Bundesanstalt für Finanzdienstleistungsaufsicht as a Crypto Trading and Custody Service provider? Based on a sample of firms, we identified over 50 potential licences that crypto providers can hold. Then we scraped the licencees of the hardest eight to obtain. This includes the FinCEN, UK FCA, Japan FSA and so on.

The graphic shows which firms hold the most licences across these eight regulators. Coinbase leads with five. Of the 100 firms we track, only 14 appear to have more than one licence. 28 hold just one. 72, nearly three-quarters, have no licence at all from these eight regulators.

This approach has proved more predictive, and there are still further regulators left to scrape. We can also look at licence withdrawals and lawsuits. Finally, there are other public data that reveal the outcomes of private ODD work, such as which firms are prepared to trade with a given counterparty. It doesn’t matter where Nexo is located. It does matter who else has given it their blessing.