Executive Summary: Stablecoin risk measures the likelihood that a stablecoin issuer or its supporting institutions fail during market stress. Institutions assess this risk using probability-of-default models, reserve quality analysis, real-time on-chain monitoring, and stress testing for liquidity and contagion. At Agio Ratings, we have proprietary models to calculate the risks of stablecoins, exchanges, and custodians in the digital assets ecosystem to enable investors to properly model their exposure to defaults.

What Is Stablecoin Risk?

Unlike holding cash, holding a stablecoin means trusting a chain of counterparties to preserve your access to funds at par value. Defaults can occur when a stablecoin issuer, custodian, or supporting financial institution fails to honor redemptions or maintain solvency during market stress.

The core components of stablecoin risk break down into four categories:

- Issuer solvency — Can the issuer redeem all outstanding tokens if everyone exits at once?

- Reserve quality and liquidity — Are backing assets liquid enough to meet redemptions without fire-sale losses?

- Redemption mechanics — Does the operational infrastructure allow for orderly redemptions?

- Regulatory and legal enforceability — Can holders actually recover assets in bankruptcy or enforcement actions?

This framework applies whether you're evaluating USDC, USDT, or any other stablecoin. The sections below break down how institutional risk teams quantify each dimension.

Why Stablecoin Risk Differs from Traditional Credit Risk

Stablecoin Risk vs. Counterparty Risk

Credit risk measures the probability a stablecoin issuer will be unable to honor redemptions. Counterparty risk encompasses all third-party dependencies, including the exchanges where you trade, the custodians holding reserves, and the banks backing those custodians.

Holding USDT exposes you to Tether's solvency. Depositing that USDT on an exchange adds exposure to the exchange's operational resilience and the custodian securing its hot wallets. Each dependency layer compounds your exposure. Agio Ratings provides credit ratings for both stablecoins and custodians, helping institutions understand their aggregated risk across the full stack.

Why Traditional Models Underestimate Stablecoin Risk

Conventional fixed-income frameworks assume a relatively high degree of continuity between reporting periods, orderly liquidation windows and regulatory oversight. Crypto markets operate 24/7 with no circuit breakers, and bank runs can materialize in hours rather than weeks. FTX faced $6 billion in withdrawals over three days before freezing accounts.

Lessons from the Terra/Luna Collapse

In May 2022, Terra's algorithmic stablecoin UST wiped out over $40 billion in under a week. The failure mechanism was simple: UST was backed by LUNA tokens, but LUNA's value derived from its convertibility into UST. When confidence broke, there was nothing underneath. Both assets spiraled to zero.

The losses weren't limited to retail money. Anchor Protocol was paying 20% yields on UST deposits, and institutional capital chased those returns. Funds parked assets there assuming "stablecoin" meant stable. Traditional due diligence didn't help as reserve attestations can't catch a flaw in the backing mechanism itself.

Measuring and Incorporating Stablecoin Risk in Models

If you're holding stablecoins, you're taking credit risk. Most models ignore this. They treat stablecoins as cash equivalents. That's a mistake. Expected loss should be modeled as a drag on returns, just like any other counterparty exposure.

Expected Loss is the Key Metric for Models

Expected Loss = Probability of Default × Loss Given Default

A stablecoin with 0.69% PD and 30% LGD costs roughly 0.21% annually. One with 0.11% PD and 20% LGD costs around 0.02%. That difference shapes how you size positions and compare risk-adjusted returns.

But these inputs aren't observable. You can't pull stablecoin PD from a Bloomberg terminal. Attestation reports show what reserves looked like 45 days ago. They reveal nothing about whether the issuer is extracting capital faster than they're building buffers.

Estimating Probability of Default

Agio Ratings’ PD estimates incorporate issuer-level financials unavailable in public disclosures or on-chain data alone: capital ratios, leverage trends, dividend extraction rates, and market risk from holdings like Bitcoin or gold. Operational tail risks—fraud, cyber incidents, regulatory action—are modeled separately since they drive most of the default probability for well-capitalized issuers.

Few risk frameworks attempt to generate forward-looking PD estimates for stablecoins due to data limitations. Agio Ratings’ models combine balance sheet signals with on-chain withdrawal patterns to estimate these risks.

Estimating Loss Given Default

LGD depends on reserve quality and legal structure. Fiat-backed stablecoins typically run 20-30% LGD—you'll recover most of your principal, but bankruptcy proceedings and liquidation costs take a cut. Algorithmic stablecoins can hit near-total loss. Terra holders recovered almost nothing.

These estimates account for factors absent from reserve composition reports: whether assets are truly unencumbered, counterparty concentration in repo agreements, and exposure to banks that might themselves face stress during a crypto drawdown.

Putting It Into Your Models

With a PD and LGD, it’s possible to run truly professional risk management:

- Set position limits as a function of PD, LGD, and concentration risk, with tighter caps for correlated or opaque reserve structures

- Compare yields on an expected-loss and stress-loss adjusted basis

- Map stablecoins to internal credit rating equivalents (with explicit downgrade triggers) to integrate them cleanly into existing mandates

The ratings translate directly: USDC maps to A-equivalent (0.11% PD), USDT to BB+ with parent support (0.69% PD) or B- without (14.55% PD). That lets you apply the same risk framework you'd use for corporate bond exposure.

Stablecoin Risk Profiles in Practice

The following examples illustrate how the framework applies to the two dominant stablecoins. For detailed credit assessments, see Agio Ratings’ full reports on Circle (USDC) and Tether (USDT), or the direct USDC vs USDT risk comparison.

Circle (USDC): Investment-Grade Risk Profile

Agio Ratings assigns Circle an A-equivalent credit rating with 0.11% annual probability of default and ~20% loss given default. USDC reserves are held in the SEC-registered Circle Reserve Fund, managed by BlackRock and invested exclusively in short-dated U.S. Treasuries and repurchase agreements.

Circle's primary risk drivers are operational tail events such as fraud, cyberattacks, regulatory sanctions rather than reserve depletion. The SVB crisis demonstrated USDC's vulnerability to banking system stress, but also showed that fiat-backed reserves enable recovery. Circle maintains capital buffers without aggressive dividend extraction.

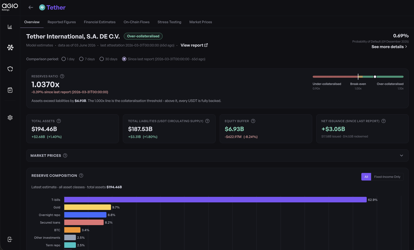

Tether (USDT): Speculative-Grade Risk Profile

Agio Ratings assigns Tether a BB+ rating with parent support (0.69% annual PD) or B- without parent support (14.55% PD). The issuer's capital ratio stands at approximately 3.7%, well below the 8% minimum required for regulated banks.

The dominant risk is structural: Tether distributed $14.2 billion in dividends over twelve months while holding Bitcoin and gold positions that amplify downside during crypto stress. Nearly three-quarters of assets are U.S. Treasuries or repos, but leverage and ongoing capital extraction create meaningful tail risk. USDT's advantage is liquidity—it maintains the deepest order books across major exchanges.

Weighing the Trade-offs

USDT offers execution advantages through market dominance but carries higher credit risk. USDC provides investment-grade safety with slightly lower liquidity and concentration in U.S. banking exposure. A trading desk might accept USDT's higher expected loss for execution benefits, while a treasury function prioritizes USDC's lower probability of default. Position sizing should reflect these credit differentials.

Monitoring Stablecoin Risk

Real-Time Liquidity Tracking

Public blockchain transparency allows institutions to observe circulating supply changes, redemption velocity, and wallet concentration patterns in real-time. Signs of an ongoing redemption wave may indicate stress or loss of confidence before it becomes public knowledge.

Agio Ratings monitors these metrics continuously for rated entities, tracking unusual outflows, changes in redemption patterns, and shifts in holder concentration. Institutions using these signals can adjust exposure before credit deterioration becomes irreversible.

Measuring Systemic Importance

Transaction flow dominance measures systemic importance and contagion risk. If a widely-held stablecoin loses market confidence, the resulting deleveraging can cascade through protocols that use it as collateral or liquidity.

Agio Ratings’ network analysis tools quantify these dependencies, helping institutions understand second-order effects beyond direct issuer exposure. A stablecoin representing 40% of DeFi collateral carries different systemic risk than one with 5% market share.

Stress Testing Stablecoin Exposure

Key Scenarios to Model

Historical scenarios like the 2022 Terra-Luna collapse and hypothetical shocks such as a 50% crypto crash quantify portfolio impact. Stress testing tools model these scenarios using calibrated probability of default increases and loss given default estimates under stress.

The Terra scenario demonstrates how algorithmic stablecoin failures can trigger contagion across protocols holding the failed asset as collateral. Institutions must model not just direct exposure but also indirect effects through counterparties and collateral chains.

Reverse Stress Testing

Working backward from insolvency outcomes identifies reserve shortfall triggers and redemption surge thresholds that would breach capital buffers. Reverse stress testing reveals vulnerabilities that forward-looking scenarios might miss.

For Tether, reverse stress testing shows the Bitcoin price decline that would exhaust capital buffers given current leverage and dividend extraction rates. For Circle, the analysis identifies the banking system stress level that would freeze redemption infrastructure.

Liquidity Assumptions Matter

Crypto market liquidity is often overestimated in stress tests. Institutions must evaluate exit timeframes and slippage costs during market dislocation, avoiding assumptions of orderly liquidation that don't hold during panics.

A position that appears liquid in normal markets can become illiquid within hours during a crisis. Stress tests should model the time required to exit at various price impact levels, informing position size limits.

Capital and Liquidity Buffer Requirements

Research shows a 2% capital requirement plus 5% liquidity reserves keep institutional default probability below 1% based on stablecoin redemption trends and fire-sale price impacts. Agio Ratings uses these benchmarks in rating methodology, assessing whether issuers maintain adequate buffers.

Capital and liquidity requirements act as substitutes for mitigating default risk from liquidity shortfalls, but as complements for limiting market spillovers from asset fire-sales. Institutions should evaluate both dimensions when setting exposure limits.

Current Regulatory Standards

The GENIUS Act

The GENIUS Act brings stablecoin transactions under Bank Secrecy Act requirements, subjecting them to the same AML scrutiny as wire transfers. Issuers must maintain 1:1 reserves in physical currency, U.S. Treasuries, repurchase agreements, and other low-risk approved assets.

Monthly public disclosures of reserve amounts, compositions, and outstanding stablecoins create standardized transparency. Issuers must have technological capability to comply with lawful orders to seize, freeze, burn, or prevent transfer of outstanding stablecoins.

Payment stablecoin issuers are treated as financial institutions, requiring effective AML and sanctions compliance programs. Foreign issuers accessing U.S. markets must meet the same standards as domestic players.

Global Regulatory Comparison

MiCA came into effect in June 2024 in the EU, introducing unified oversight with similar reserve and transparency requirements. The convergence of U.S. and EU standards creates a global compliance baseline for institutional-grade stablecoins. Financial Stability Board recommendations emphasize that reserve assets should be unencumbered and immediately convertible into fiat at minimal loss—principles now embedded in both frameworks.

Institutional Stablecoin Risk Management: Best Practices

Once probability of default and loss given default are quantified, institutional risk management becomes an execution problem rather than a conceptual one.

Due Diligence Checklist

Comprehensive assessment evaluates regulatory licensing, financial health metrics, operational resilience, and custody arrangements. A structured rating methodology covers these dimensions through quantitative probability of default models.

Financial due diligence examines capital ratios, profitability, dividend policies, and reserve quality. Regulatory licensing assessment verifies compliance with applicable frameworks including the GENIUS Act and MiCA. Operational resilience testing evaluates redemption infrastructure capacity under stress.

Continuous Monitoring Beats Point-in-Time Reviews

Real-time treasury tracking with threshold-based triggers outperforms quarterly snapshot reviews. Continuous monitoring detects deteriorating conditions months before they become visible in periodic disclosures.

Continuous tracking rather than point-in-time diligence often determines whether you exit before collapse or get trapped in bankruptcy proceedings. Institutions should implement automated alerts tied to probability of default thresholds.

Stablecoin Risk in Portfolio Allocation

Matching Risk Tolerance to Stablecoin Selection

Institutional mandates determine appropriate credit-quality tiers. Treasury management functions with conservative mandates should concentrate in A-rated issuers like Circle. Trading operations accepting higher risk for liquidity benefits might allocate to BB+-rated issuers like Tether with appropriate position limits.

Agio's rating scale enables consistent mapping between institutional risk tolerance and stablecoin selection. Investment committees can establish clear policies linking credit ratings to maximum exposure levels.

Pricing Counterparty Risk into Returns

Subtracting expected loss (probability of default × loss given default) from stablecoin yield calculates risk-adjusted net return. A stablecoin offering 5% yield with 0.21% expected loss provides 4.79% risk-adjusted return.

This methodology enables apples-to-apples comparison across stablecoins with different credit profiles. Institutions can optimize allocations by selecting the highest risk-adjusted returns within their risk tolerance bands.

Position Sizing Based on Default Probability

Exposure limits should be inversely proportional to probability of default. An institution might cap USDT exposure at 25% of stablecoin holdings while allowing 75% in USDC, reflecting the credit differential quantified by Agio Ratings.

Position sizing rules should incorporate correlation with existing exposures. If an institution already has significant exposure to the U.S. banking system, USDC's concentration in systemically important bank deposits warrants lower position limits.

Hedging and Insurance Options

Insurance products enable institutions to transfer tail risk while maintaining operational exposure. Relm Insurance offers crypto exchange default coverage powered by Agio Ratings, providing a practical mechanism for managing extreme scenarios.

Hedging strategies should focus on catastrophic outcomes rather than routine volatility. The cost of insurance or hedging must be weighed against the expected loss reduction to determine whether risk transfer improves risk-adjusted returns.

Frequently Asked Questions

Why did proof-of-reserves fail to prevent FTX and other collapses?

Proof-of-reserves provides snapshots that can be manipulated through temporary borrowing and ignores liabilities entirely. A custodian might hold $1 billion in assets but owe $2 billion, appearing solid while insolvent. The approach doesn't capture off-chain obligations or ongoing financial health. Agio's continuous monitoring addresses these gaps by integrating balance sheet data, on-chain behavioral signals, and forward-looking statistical models—detecting deterioration months before it shows up in quarterly attestations.

Are algorithmic stablecoins riskier than fiat-backed stablecoins?

Yes. Algorithmic stablecoins rely on circular backing mechanisms vulnerable to confidence loss, while fiat-backed stablecoins maintain reserves of dollars or equivalents. Terra's UST demonstrated near-total loss given default when its algorithm failed, whereas fiat-backed stablecoins typically show 20-30% LGD reflecting reserve liquidation costs.

What stress testing scenarios should institutions use for stablecoin portfolios?

Historical scenarios like the Terra collapse and SVB banking crisis, plus hypothetical shocks such as 50% crypto crashes or major issuer hacks, calibrate institutional risk appetite. Models should account for both direct exposure and indirect effects through counterparties and collateral chains. Agio's stress testing tools model these scenarios using calibrated probability-of-default increases and loss-given-default estimates under stress.

How does USDC differ from USDT in terms of institutional safety?

USDC earns an A-rating with 0.11% annual probability of default, while USDT carries a BB+/B- rating with 0.69-14.55% PD depending on parent support. USDC's primary risks are operational tail events, while USDT faces leverage, market exposure to Bitcoin and gold, and ongoing dividend extraction that limits capital buffers. For a detailed breakdown, see Agio's full USDC vs USDT risk comparison.

How can institutions monitor stablecoin risk in real time?

Public blockchains provide transparency into circulating supply, redemption velocity, and wallet concentration but interpreting these signals requires context. Agio Ratings monitors these metrics continuously for rated entities, tracking unusual outflows, redemption pattern changes, and holder concentration shifts. Institutions using Agio Ratings’ platform receive alerts when risk indicators breach predefined thresholds, providing time to adjust exposure before credit deterioration becomes irreversible.

Where can I get credit ratings for stablecoins?

Agio Ratings publishes independent credit risk assessments for stablecoin issuers, custodians, and exchanges. Ratings include probability of default, loss given default, and expected loss metrics mapped to traditional credit rating equivalents—enabling institutions to integrate stablecoin exposure into existing risk frameworks. Book a demo to see how Agio Ratings’ platform can support your risk management process.

Building a Stablecoin Risk Framework

Institutional stablecoin risk management requires combining traditional credit analysis with crypto-native monitoring. Assess probability of default and loss given default using statistical models that integrate balance sheet health and on-chain behavioral signals. Monitor continuously rather than relying on quarterly snapshots. Stress test exposures against both historical crises and hypothetical shocks. Apply position limits inversely proportional to credit risk.

The framework synthesizes into a repeatable process: evaluate issuers using quantitative credit ratings, track real-time liquidity and redemption patterns, model portfolio impact under stress scenarios, and size positions based on risk-adjusted returns within institutional mandates. Institutions that implement this process can participate in digital asset markets while maintaining defensible risk management standards.

Agio Ratings provides the tools institutional risk teams need to implement this framework. Our probability-of-default models, continuous monitoring systems, and stress testing tools enable banks, trading firms, and insurers to quantify, compare, and actively manage stablecoin counterparty exposure using methods aligned with traditional finance risk frameworks.