The best way to manage financial risks in digital assets

Agio Ratings provides a suite of risk management tools for institutions to assess, monitor and model financial risks in digital assets.

Trusted by the most sophisticated risk teams in digital assets

The Problem

Traditional risk models don’t work in a market as dynamic, fragmented, and opaque as digital assets.

The Solution

We continuously monitor on- and off-chain risk factors correlated with default risk.

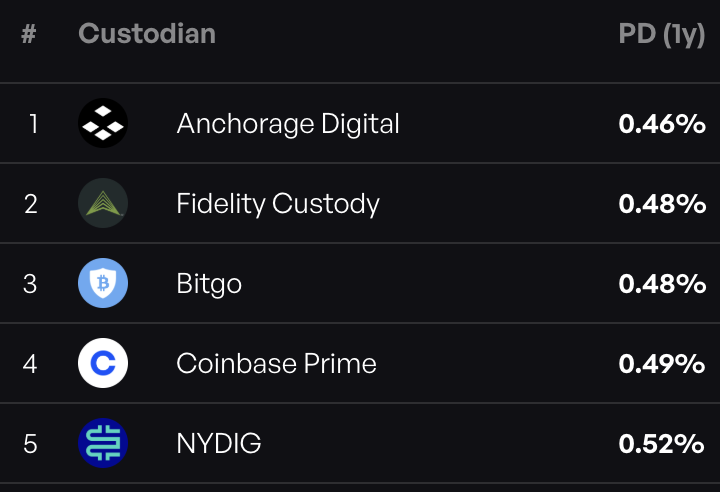

70+ Exchanges and Custodians Rated

Reliable default probability analysis

Comprehensive Risk Models

More precise and transparent than existing solutions

80+ Financial Firms Monitored

Real-time transaction tracking

Platform

Agio Ratings Features

Monitoring

Track on-chain risk signals in near real-time.

Monitoring

Track on-chain risk signals in near real-time.

Modeling

Convert any probability of default for a portfolio of counterparties into a loss distribution.

Modeling

Convert any probability of default for a portfolio of counterparties into a loss distribution.

What our clients say

“...Their risk alerts allow proactive risk mitigation, and we've recently added their Risk Simulator to model broader risk events. We highly recommend Agio Ratings for those focused on comprehensive risk management.”

Bernard Orenstein

CEO of Sharewell

"Agio Ratings' risk platform offers real-time, advanced assessments of key counterparties and has enhanced our methodology for managing portfolio..."

John Glover

Chief Investment Officer at Ledn

“Growing institutional participation is creating a greater need for credible, independent risk intelligence. Agio Ratings provides a clear, data-driven view of the probability of default for exchanges and other institutions, and their alerts deliver a valuable independent signal alongside our own monitoring.”

Alain Passini

Head of Risk at Wintermute

"We’ve long believed that institutional investments in digital assets require robust counterparty risk management. That's why we apply rigorous controls and equip our risk team with best-in-class infrastructure. Agio Ratings helps us to maintain the strong risk posture that’s required for success."

Stefano Ruggiero

COO of Abraxas Capital Management

“I highly recommend Agio Ratings' services to those seeking a trusted partner in ratings and risk assessment.”

Dr. Claire Davey

Head of Product Innovation & Emerging Risk

Backed by leading investors

Subscribe to our monthly risk briefing

Your trusted source of credit insights for the digital asset market, serving market makers, funds, regulators, banks and insurers.

Manage risk professionally

Agio Ratings helps financial leaders make smarter, data-driven decisions in the evolving digital assets landscape. Protect your capital, optimize underwriting, and stay ahead of market risks.